Semiparametric Estimation of Fractional Integration: An Evaluation of Local Whittle Methods

Jason R. Blevins.

The Ohio State University, Department of Economics

Working Paper.

Availability:

- Working Paper (updated July 20, 2026)

- arXiv (updated July 20, 2026)

- Replication Code

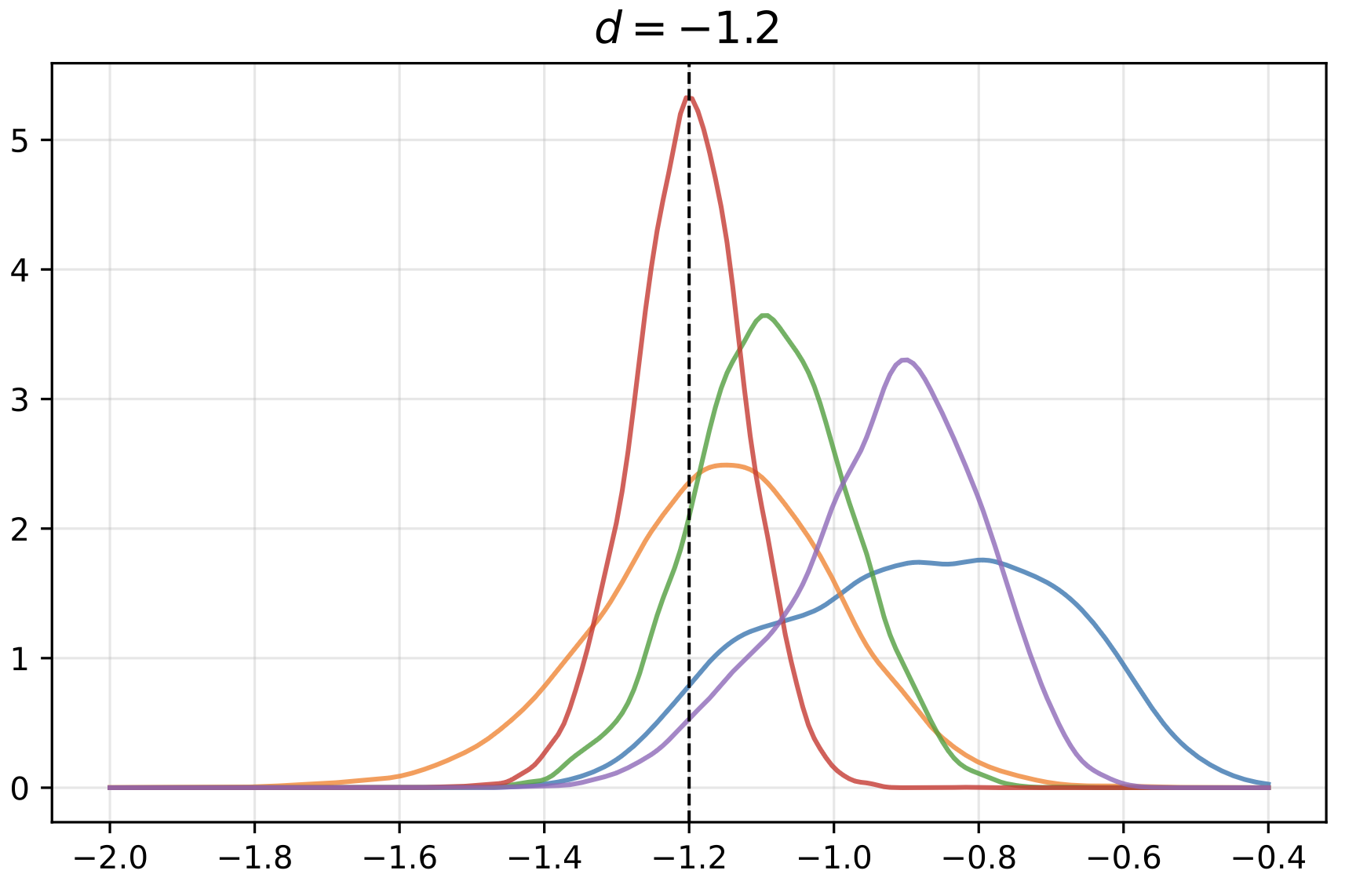

Abstract. Fractionally integrated time series, exhibiting long memory with slowly decaying autocorrelations, are frequently encountered in economics, finance, and related fields. Since the seminal work of Robinson (1995), a variety of semiparametric local Whittle estimators have been proposed for estimating the memory parameter , each with a distinct range of validity and different robustness properties, leaving applied researchers to decide which to use and under what conditions. This paper offers a practitioner’s guide to six such estimators. Using a common Monte Carlo design, we map how each estimator behaves under short-run dynamics, unknown means, and time trends—the conditions under which each remains reliable and the characteristic way each breaks down. This reveals a tension between efficiency and robustness: the exact local Whittle estimator uniquely pairs the lowest asymptotic variance with an unrestricted parameter range, but requires the mean and trend to be handled with care. We then illustrate these failure modes, along with the difficulties introduced by structural breaks, on several macroeconomic, financial, and climate time series, where a naïvely applied estimator can report near-stationarity for a series that better-matched methods identify as strongly nonstationary. The resulting guidance on estimator choice and bandwidth selection is anchored by exact reproductions of published results from this literature, along with open source replication code and datasets.

Keywords: fractional integration, long memory, nonstationarity, semiparametric estimation, local Whittle estimation, exact local Whittle estimation.

JEL Classification: C13, C14, C22, C52.

BibTeX Record:

@TechReport{blevins-2026-lws,

author = {Jason R. Blevins},

title = {Semiparametric Estimation of Fractional Integration: An Evaluation of Local {Whittle} Methods},

type = {Working Paper},

institution = {The Ohio State University},

year = 2026,

archivePrefix = {arXiv},

eprint = {2511.15689}

}